Hiking and Adventure Sports Insurance

One of the most common enquiries I get from my readers is about hiking insurance. Do I need it? Quite possibly. Is it necessary over and above travel insurance already purchased at home? Maybe as some travel insurance policies stipulate hiking under 2000 metres altitude. Are there local companies that you’d recommend for people coming from abroad? There are a couple, but you need at least a rudimentary grasp of Japanese plus the help of Google Translate, as their websites are only in Japanese. What is the cost of a helicopter rescue in Japan? Deploying a helicopter for example, in Saitama Prefecture (it varies according to the prefecture) costs 60,000 yen per hour. To name but a few.

If there is any doubt as to the need to take out hiking insurance I suggest first reading this post “Hiking in Japan: Why Insurance Matters” which cites an average rescue cost of ¥398,000 ($3,500 USD). Also, according to this Nippon article, there were around 3,100 mountain-related incidents involving over 3,500 people across Japan in 2023.

For long-term residents in Japan, numerous hiking insurance options exist, covering everything from search and rescue to hospitalisation, liability, death benefits, and overseas activities. For short-term visitors to Japan planning a hiking adventure, I highly recommend taking out travel insurance that covers search and rescue, at least as a minimum. The TOKIO OMOTENASHI POLICY is a great option, as it’s tailored specifically for foreign visitors and offers affordable short-term coverage plans ranging from 1 to 31 days.

Hiking Insurance Providers in Japan at a Glance (2026)

| Insurance Provider | Cost | Insurance period | How to apply | Activities covered | Other details |

|---|---|---|---|---|---|

| COCOHELI | ¥6,600 plus a one-time enrolment fee of *¥3,300 | 1 year | Online | Hiking / mountaineering and various outdoor sports | Search and rescue up to ¥5.5 million / indemnity liability |

| TOKIO OMOTENASHI POLICY | ¥800 to ¥9,420 | Up to 31 days | Online | Hiking and various outdoor activities | Search and rescue up to ¥10 million / hospitalisation / death and disablement |

| YAMAP hiking insurance | ¥580 to ¥5,840 | 1 year and short-term 7 or 30 days | Online | Varies according to the plan | Search and rescue up to ¥3 million |

| Montbell | From ¥8,270 for a basic "climbing" and ¥2,930 for a basic “outdoors” | 1 / 3 / 5 years | Online | Varies according to the plan | Search and rescue up to ¥5 million / hospitalisation / death and disablement / indemnity liability |

| Nihon Hiyo Hosho | ¥4000 | 1 year | Online | Varies according to the plan | Search and rescue up to ¥5 million / indemnity liability |

| Yamakifu | ¥660 to ¥10,000 | 1 year and short-term 1-4 days | Online | Varies according to the plan | Search and rescue up to ¥5 million / indemnity liability |

*If you sign up through their friendship program and use my code “26831” (ご紹介用クーポンコード: referral code), you can save the enrolment fee.

1. COCOHELI

In July 2022, COCOHELI and jRO merged, with jRO becoming a wholly-owned subsidiary of COCOHELI. In addition to COCOHELI’s membership-based helicopter search service, jRO’s search and rescue service was integrated. Along with hiking and mountain climbing, it also provides coverage for trail running, rock climbing, sports climbing, bouldering, skiing, snowboarding, mountaineering, canyoning, caving, and mountain biking. Search and rescue expenses are covered up to 5.5 million yen. If you sign up through their friendship program and use my code “26831” (ご紹介用クーポンコード: referral code), you can save the enrolment fee (3,300 yen).

Pros: Membership benefits include discounts at some mountain huts and a radio transmitter.

Cons: Most plans don’t cover death and disablement, injury, or hospitalisation.

2. TOKIO OMOTENASHI POLICY

TOKIO OMOTENASHI POLICY, underwritten by Tokio Marine & Nichido Fire Insurance Co., Ltd., is designed specifically for short-term travelers to Japan. Unlike Yamakifu’s policy, which requires policyholders to maintain a domestic residence, TOKIO OMOTENASHI POLICY doesn’t have this requirement, making it a good option for travelers without a Japanese address. While it covers search and rescue if the police or other public agency has deemed such operation necessary, there are exclusions. It won’t cover activities requiring climbing equipment, including the use of crampons and ice axes or altitude sickness developed during mountain climbing. Coverage begins from ¥800 yen up to ¥9,420 yen for 31 days (maximum duration for this policy).

Pros: Best travel insurance option for short-term travellers covers most hiking activities.

Cons: Only covers trips up to 31 days.

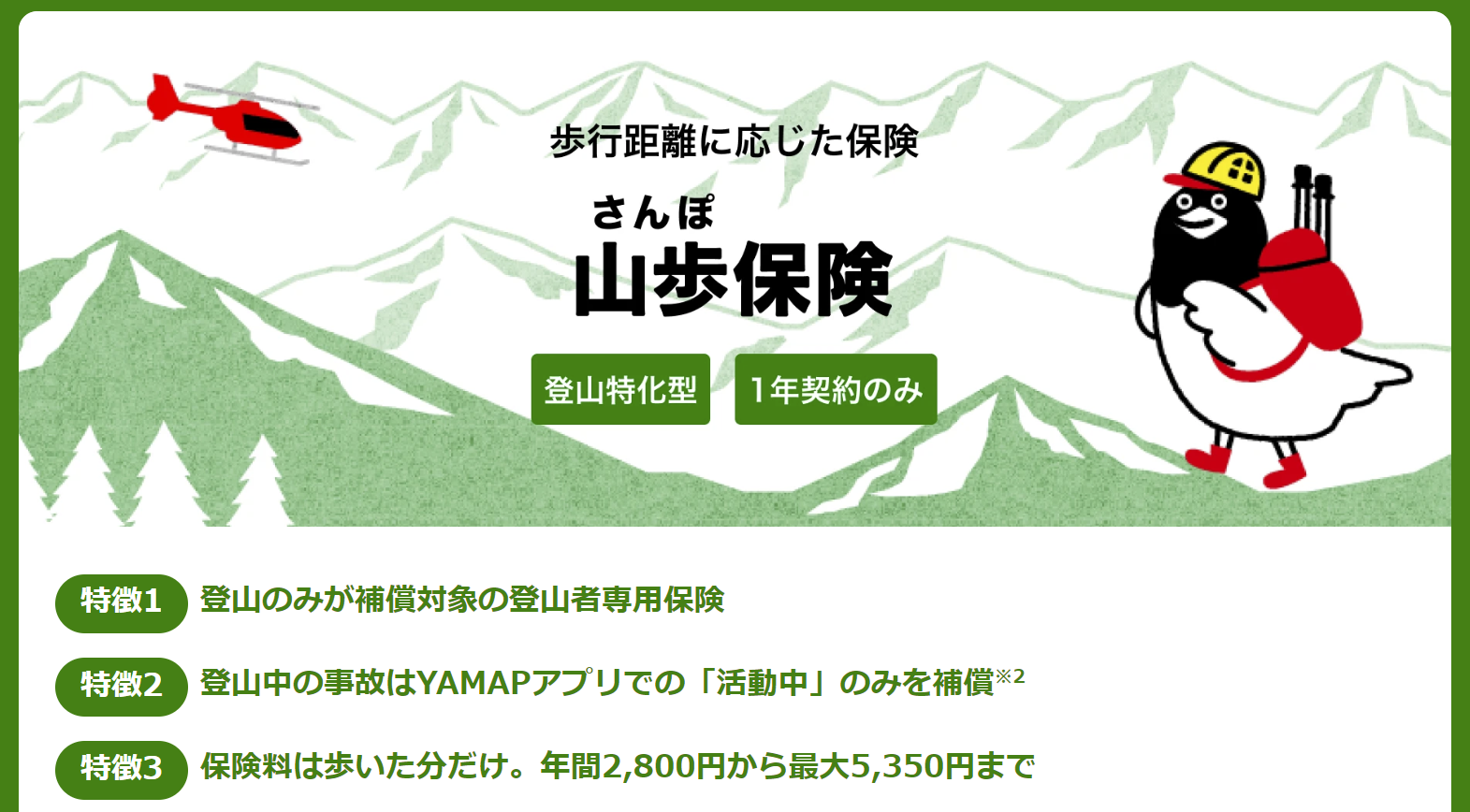

3. YAMAP hiking insurance

YAMAP, the popular SNS and GPS tracking service for hikers in Japan, offers two types of hiking insurance: 山歩保険 (Sanpo Insurance) and 外あそびレジャー保険 (Outdoor Leisure Insurance). You do not need a paid YAMAP Premium membership to purchase either plan, but: A YAMAP account and the YAMAP app are required to activate Sanpo Insurance coverage during hikes. Sanpo Insurance coverage is only valid if you use the app to record your hike. Outdoor Leisure Insurance does not require app usage.

Sanpo Insurance is an annual plan only (not 7- or 30-day).

Outdoor Leisure Insurance offers 7-day, 30-day, and annual options.

Sanpo Insurance (Hiking-Only)

• Covers search and rescue expenses up to 3 million yen

• Annual plan only (price based on distance walked in YAMAP app)

Outdoor leisure Insurance

• Includes limited liability as well as search and rescue expenses

• Available in 7-day, 30-day, and annual plans

Usage Requirements for Sanpo Insurance (Hiking-Only)

To activate coverage, you must:

1. Download a map in the YAMAP app before starting your hike

2. Tap “Activity Start” before your hike and “Activity End” afterward

3. Use the same YAMAP account for both the app and insurance purchase

4. Keep GPS tracking enabled during your hike

Outdoor Leisure Insurance

This plan does not require the use of the YAMAP app and covers:

• Hiking, skiing, snowboarding, trail running, cross-country skiing

• Certain daily-life injuries

• Greater flexibility for those engaged in a range of outdoor activities

Pros:

Flexible coverage periods (7-day to annual). Injury compensation up to 300,000 yen. Coverage includes expenses for relatives to travel to the scene of an accident or disaster. Outdoor Leisure Plan offers broader activity coverage beyond hiking.

Cons:

Sanpo Insurance requires strict YAMAP app usage to activate coverage. No coverage for death, permanent disability, hospitalization, or third-party liability. App-based tracking may be unreliable in areas with poor GPS reception.

4. Montbell hiking insurance

Clothing and equipment behemoth Montbell provides comprehensive insurance coverage underwritten by AIU Insurance. They offer two plans: “outdoors” and “climbing”. The outdoor plan (general injury insurance) covers activities such as trekking, hiking, camping, cycling and skiing, while the climbing plan (comprehensive insurance) covers full-fledged mountaineering. On top of this, Montbell offers a bewildering 90 different coverage types ranging from one to five years, with the more expensive plans covering hospitalisation expenses, indemnity liability, death and disablement. The annual premium for a basic plan “climbing” is 8,270 yen, which can be purchased on the internet and is valid from the afternoon of the next day.

Pros: Some plans cover trekking and outdoor activities while abroad. A wide variety of plans to select from.

Cons: Expensive when compared with other insurance providers.

5. Nihon Hiyo Hosho hiking insurance

Nihon Hiyo Hosho or Nihiho offers affordable “rescue cost insurance” for hiking and various outdoor sports, including rock climbing, trail running, backcountry skiing, snowboarding, canoeing and mountain biking. The 4,000 yen annual fee covers expenses required for search and rescue including helicopter callouts up to 3 million yen. The policy starts at midnight on the day following payment.

Pros: Relatively inexpensive at 4,000 yen or only 333 yen per month.

Cons: Death and disablement, hospitalisation and indemnity liability are not covered.

6. Yamakifu hiking insurance

Based out of Chiba, Yamakifu is one of the few outfits that also offers short-term hiking insurance. The basic annual fee is 4,000 yen and covers search and rescue expenses up to 5 million yen. There is also a plus members category for 7,500 yen that includes indemnity liability, limited hospitalisation expenses, and outpatient care. The expert member fee is 10,000 yen and covers mountaineering and ice axe use. The “one-time” short-term insurance ranges from day trips (660 yen), 2 days (990 yen), up to 4 days (1,600 yen) and provides coverage similar to the plus members category.

Pros: The plus and expert plans cover mountain climbing or hiking while abroad. Competitive rates and good coverage combined with short-term plans. Some plans cover injuries caused by natural disasters.

Cons: Travellers must have a domestic residence, not a hotel or short-term accommodation. Need to submit a hiking plan to guarantee you are fully covered.

Really appreciate this, I think I’ll go with jro.

Being a long time resident in japan, I’ve just taken up hiking and your site has helped me out a lot!

Thanks, and good to hear it. jRO are a solid outfit and I’ve been a signed up member with them for many years.

Is Yamakifu and YAMAP still available for tourists?

I can stumble my way through websites in Japanese and signup for many things, but its hard to search and check all the conditions.

Agree it’s hard to keep up to date with these insurance providers. YAMAP still have their rescue plan 480 yen per month (renews automatically every 30 days) or 650 yen per month with equipment coverage for smartphones, skies, snowboards etc. They also now offer affordable daily rates at 280 yen per day. Yamakifu’s plans remain unchanged at 660 yen per day; 990 yen for 1 night 2 days; and 1600 yen for 3 nights 4 days. And yes, these hiking insurance policies are available for purchase by international visitors.

Thanks for the great post David.

Yamakifu might not be suitable for tourists. Last year I was able to get insured with my hotel address, but this year they have cancelled my application and one-time membership for not having a domestic residence (juusho 住所). The clause is also cited on their website’s Q&A, so there is a risk of claim denial for shot-term visitors.

Yamakei recommends TOKIO OMOTENASHI POLICY for visitors, said it covers search and rescue expenses. However, no such information could be found on the insurance company website.

Yamakei’s “Hikes in Japan”: https://hikesinjapan.yamakei-online.com/information/l.php

Hi Peter,

Thanks for the heads up. It’s a little disappointing, as I know Yamakifu was very convenient for short-term stayers like yourself.

I just had a look at Tokio Marine & Nichido Fire Insurance’s TOKIO OMOTENASHI POLICY (Japanese version). From what I can tell, it does provide partial coverage for hiking activities, provided they don’t fall under what they refer to as 危険な運動 (Kiken na undō) or dangerous activities, such as the use of climbing equipment like ice axes, crampons, climbing ropes, mountaineering equipment etc. They also won’t pay insurance benefits incurred due to altitude sickness developed while the insured person is engaged in mountain climbing. But as you say doesn’t mention whether it includes search and rescue.

A small update: I have found the provision in their terms of conditions, at the bottom of the company’s webpage (p. 12-13 in English, and 36-37 in Japanese).

So yes, TOKIO OMOTENASHI POLICY does cover emergency search and rescue expense, if the police or other public agency has deemed such operation necessary. Like you said, altitude sickness is not covered (p. 14-15, 38-39).

Thanks for clarifying this. I followed up with them via email today and received the same confirmation.

If you live in Japan and already have shakai hoken, do you need to take out specific insurance for hospitalization or injuries caused up in the mountains? If not, then just search and rescue seems enough right?

If you have shakai hoken it should cover any hiking related medical expenses. In this case you’d probably be fine with just a search and rescue plan.

Still a classic post, David! Any recent developments you know of regarding options that provide service and sign-up in English?

Thanks for that Rob. To the best of my knowledge none of these insurance providers offer service and sign-up in English. I guess they anticipate international visitors will buy insurance in their home countries and long-term stayers can manage the sign-up in Japanese.

Thanks David!

Hi David! It’s such a helpful article about mountain insurance!

By the way my friend, a reader of this article, gave me an idea that it will be even more comprehensive article if you add information about CocoHeli! Cocoheli is a membership-based helicopter search service for mountain distress such as getting lost and slip / drop accidents. You will get a small radio transmitter which can be detected up to 16km. In case you are missing, your family or friend calls the cocoheli center and a helicopter will be sent to search for your beacon. Note you can’t request the helicopter by yourself (unless you have cell phone signal to call the cocoheli center) Also it’s a collaborated service with jRO, for example if you have jRO insurance then you don’t need to pay application fee for Cocoheli.

I hope this helps to improve your article and give more information for your readers!

https://hitococo.com/cocoheli/

Hi Shihori san,

Thank you for your comment and suggestion about including the Cocoheli helicopter search and rescue service. What I might do is write a separate blog post about Cocoheli and how it operates as I’m sure it’s of interest to my readers. Including for example, its range as you mention 16km, areas of Japan it covers (currently 34 prefectures and most mountainous areas as at Sep 2020), cost ~3,650 yen and tie-ups with other mountain insurance providers.

That’s great!

Thank you David san!

In reading the terms of use, I noticed that jRO seems to require annual ex-post contributions in addition to the annual fees (on a pro-rata total reimbursements/total members basis). While I understand this obviously varies year to year, can you shed some light on how much this tends to run annually? (I’ve been using a different provider until this year, but am considering a switch to jRO because you and some hiking friends of mine all seem to like it.) Thanks in advance!

Hi Susan and thanks for your comment. Yes, you are correct the annual member contribution fees fluctuate each year according to ex-post contributions which is usually between 300-800 yen. Having said that most years include an adjustment which reduces this amount for 2019 and 2020 members had to pay an additional 200 yen. For 2008-2018 jRO outlines it on their website here.

Thank you! This answers my question perfectly – and thanks for the website link too. I looked for that information on the jRO website but couldn’t find it (probably more due to my Japanese, which is far from perfect, than to it being difficult to find). Most excellent. I will sign up with them shortly. Thanks for this website too – it’s one of the absolute best resources around.

I tried looking at several of the insurance options but they all seem to require you to have a Japanese address which means you need to be a Japan resident. Do you know of any that will allow foreign tourists to buy insurance? I come to Japan to visit family twice a year so I would buy an annual plan. Thanks.

To acquire a hiking insurance policy in Japan it needs to be tied to a Japanese mailing address. For short-stay foreign tourists taking out a policy, say with Yamakifu this could include your hotel or short-term accommodation. As you have family here and intend to buy an annual plan, your best bet would be to use their Japanese mail address. They could in turn notify you of or forward to you any correspondence they receive on your behalf, such as your JRO insurance card.

In looking into insurance for my summer hiking adventures in the genryu areas, I excitedly read this post and am so grateful for the info. I was looking into YAMAP, but then I saw that they’ve discontinued their mountaineering insurance (not sure if they still have a general “outdoor” insurance or not): https://info.yamap.com/archives/319

JRO (according to Google Translate) covers mountain stream fishing specifically, so I’ll likely go with them.

Thanks for all the outstanding information!

Thanks for the heads-up regarding YAMAP discontinuing their hiking insurance. I have updated the post to reflect this new information. JRO is a solid choice, and I am pleased to hear that they cover your needs.

Hi,

Myself and 2 of my teenage boys are planning to hike Mt. Fuji in Aug, 2025. Just to be safe I would like to get a hiking insurance. Looks like provided info is in Japanese. Can I find any info in English, please?

Thank you,

Alla

Hi Alla,

For overseas travel insurance, I recommend obtaining a policy from a provider such as World Nomads or Insured Nomads. Their policies typically cover overseas medical expenses as well as mountain accident insurance.

Alternatively, you may want to consider the TOKIO OMOTENASHI POLICY (you can sign up in English using the link in the post above). This travel insurance also covers search and rescue if the police or another public agency deems such an operation necessary. However, it does not cover altitude sickness developed during mountain climbing.

Was looking at Insurance because I was prompted whilst using the Yamap app. It appears they have a new offering, ¥2800 for a year (It increases after 1 year).

Covers injury, rescue, and legal indemnity.

Thought I’d let you know in case you revisited.

Thanks for the heads-up! I’ve updated the post accordingly.